Central Oregon Housing Market Update, June 2026: What's going to happen to rates through the rest of the year?

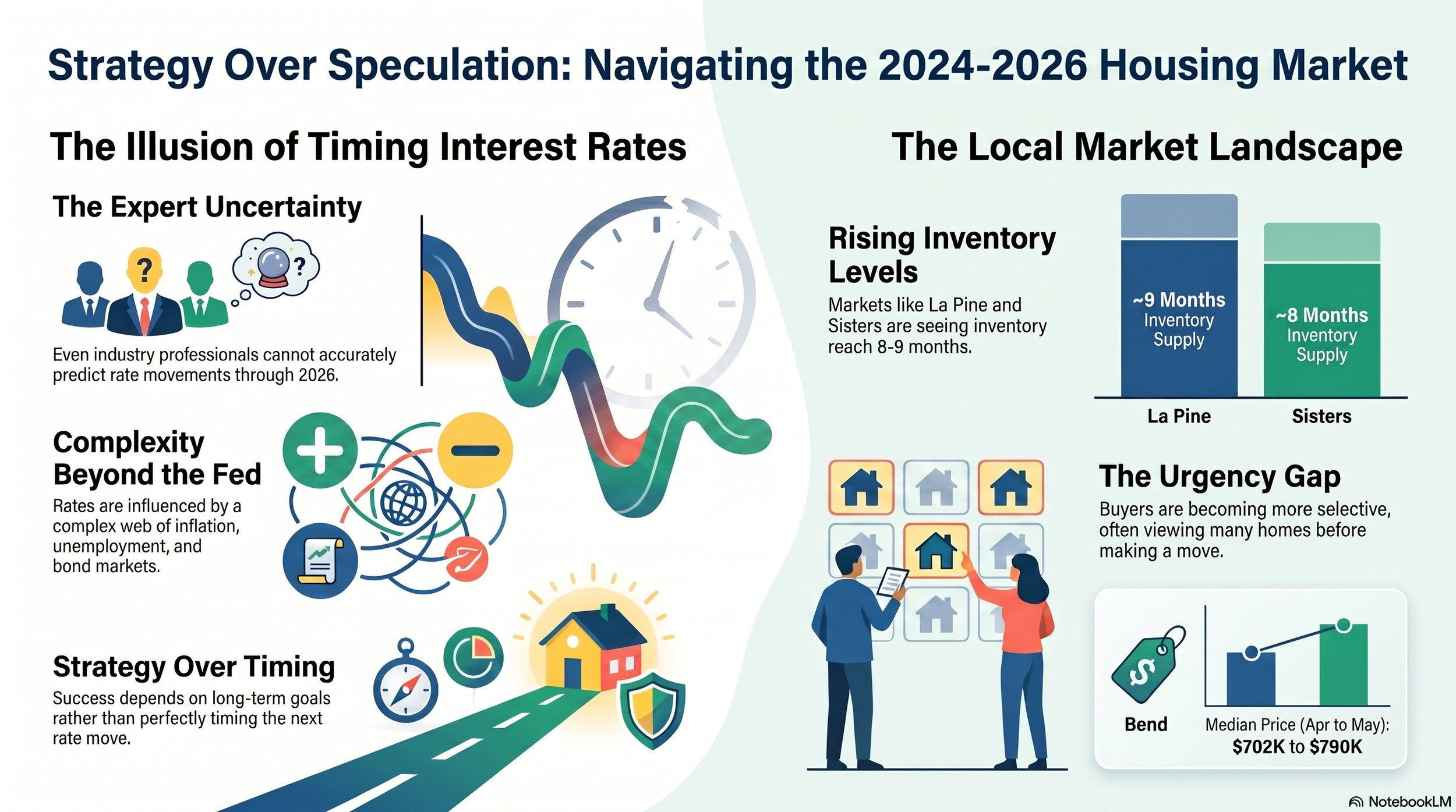

That question was posed by a mortgage officer to a room full of real estate agents I was sitting amongst last week. It was a fitting question, and a good reminder that even those who spend every day working in housing and lending don't know the answer. The reality is that nobody does.

There was some discussion about rates potentially moving lower following the appointment of a new Federal Reserve Chair and the public pressure from President Trump to lower interest rates. While I'll spare you the Schoolhouse Rock! version of how the Federal Reserve doesn't directly control mortgage rates, it is a good reminder that the relationship between inflation, unemployment, Federal Reserve policy, bond markets, and mortgage rates can be incredibly complex. Even those who live and breathe this stuff seven days a week don't always agree on what happens next.

That uncertainty has certainly found its way into the local housing market.

Questions like, "Should I wait?" remain common among buyers. Those who are ready to move forward are often finding themselves adjusting their price range to accommodate mortgage rates that have returned to the mid-6% range. Sellers, meanwhile, appear more motivated to make a move. I touched on this in last month's newsletter when discussing markets like La Pine, which is sitting at roughly 9 months of inventory, and Sisters, which remains around 8 months. Redmond has also seen inventory build much faster this year than it did last year.

At the same time, buyers generally don't feel the same urgency they did a few years ago. If they find a home they like, many are willing to look at another ten before making a decision, even if it means losing out on the first one. Others are content to wait and see if a seller eventually reduces the price before making a move.

Despite that dynamic, homes continue to sell at a fairly steady pace. What has changed is where buyers are choosing to buy. Bend's median sale price jumping from $702,000 in April to $790,000 in May is one of the more obvious examples of how shifts in buyer activity can dramatically impact the headline numbers.

So what do I think happens with rates through the rest of the year?

My educated guess is that they remain somewhere near where they are today. There are simply too many unknowns still at play for the broader market to confidently push rates meaningfully lower. I'd be more than happy to be wrong if rates improve as the year progresses. Until then, having a strategy and understanding when buying or selling does and does not support your long-term goals will remain far more important than trying to perfectly time the next move in mortgage rates.